Southeast Asia is one of the fastest growing regions in the world nowadays, that’s why it is important to talk about the financial side of it. And if we are going to talk about it, then we have to talk about loans.

This article will serve as an overview to how lending money works in this part of the world. And even though we won’t talk about all the countries, we will talk about the most important ones like Singapore, Thailand and Vietnam.

A Curious Case:

It is not only individuals and businesses that are requesting loans. If we look back to March 2016, we will discover that China offered $11.5 billion in loans to this region, mainly focused on infrastructure.

This was a very smart and necessary offer, because one of the main obstacles stopping countries like Vietnam, Laos and Thailand from growing properly is the lack of funds for building better roads, ports and railways, all of which are necessary for growth.

This is a curious case which allows us to see that not only individuals and businesses are interested in taking loans.

Cash Cards: More Available Than Ever Before

Cash Cards: More Available Than Ever Before

One of the many things that stops several individuals, students and business owners from getting a loan is that they have no credit history, and hence, it’s almost impossible for a bank to grant it without attaching hefty fees to it.That’s why cash cards like Umay Plus from Thailand are quickly becoming very popular, because their requirements are not very demanding and their interest rates are excellent.

If we analyzed Umay Plus, we would find that Thai residents who earn more than 7000 THB per month can get their own Umay Plus Card. Moreover, the interest rates are never higher than 15%, which is a great advantage.

Moreover, they bring multiple solutions to their clients: you can pay the full amount, the half or the lowest fee. You decide.

And just like Umay Plus in Thailand it is possible to find similar options in other countries like Indonesia, Vietnam, Singapore and the Philippines.

And as you can easily tell, cash cards are more popular amongst individuals, because for business owners it is not enough. Launching a business or start-up with the help of cash cards is way too demanding and not a good idea at all. But that’s why P2P lending platforms exist.

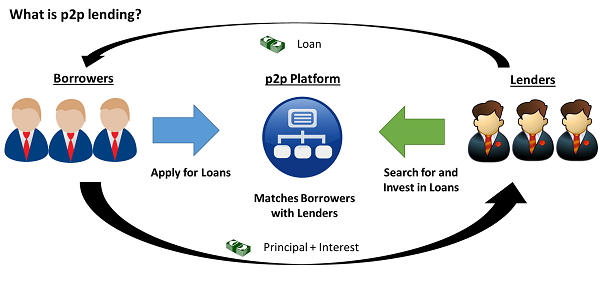

The Revolution of P2P: Lending Made Easy

A recurrent problem across all Asian countries is that many persons don’t have a credit history, and hence, it is very hard to get a loan from a formal institution like a bank.

This is a problem, and a pretty big one, and that’s what several Fintech startups have seen as an opportunity, because by taking down the barriers that stop individuals and business owners in Southeast Asia from getting a loan, they can enter that market. And that’s exactly what they’ve done.

A New yet Promising Market:

Even though P2P lending platforms address a very serious problem and bring a solution to it, it is still early in its development in the region.

For example, if we compare it against China which has excellent P2P platforms like CreditEase, we will find that 10% of loans are originated from P2P lenders, whereas in Southeast Asia that number barely reaches a 0.1%.

As you can see, in comparison to China, it is still very young. But this type of solution has a bright future in the region, let’s find out why.

Consuming Class: The Fuel

What will ignite the growth of P2P lending in Southeast Asia to the next level? The answer is the young and growing consuming class.

It is calculated that 4-5 million persons will be joining the consuming class every single year. These persons are driven by consumerism, which will motivate them to obtain loans in order to improve their lifestyle.

And even though not all of them will resort on P2P, it is expected that a large number will do. After all, the most attractive options are this one and cash cards like Umay Plus which make it easy for young people to get them.

This young working and consuming class will not only ignite the growth of P2P lending in the region, but boost its economic growth in all senses.

P2P lending solves a big problem, and as it seems, the demand for this type of solution will grow year by year. That’s why it is just a matter of time for these platforms to experience a massive growth.

Small and Micro Businesses:

If we take a closer look we will also find out that the small and micro businesses in Southeast Asia will play a big role in the development of this kind of lending. It is due because a big part of owners of this kind of businesses are considered unbanked, and hence, it is impossible for them to get a loan from a bank or any other formal institution.

Where will they resort then? You already know it: P2P. It is very probable that will follow China’s example.

More often than not their monetary requirements are not very high, so it will be easy for these P2P platforms like MoolahSense and Funding Societies to meet their needs.

Dealing with Loansharks:

The phenomenon of unbanked individuals in this region of the world is interesting, and if we look closer, we will find out that many times they resort on “loansharks” to get the funds they need, and it doesn’t matter if their life is at risk and the fact that they have to pay extremely high fees.

Once again, P2P lending will help to deal with this problem. By allowing the unbanked to access a different and much better way of getting a loan, it is obvious that less of them will resort on loansharks.

Conclusion:

As we can see the loans panorama in Southeast Asia is quite interesting. There are several problems, but fortunately, the solutions have started to appear.

{kind=link}